Taxes for new homeowners

When and how should you pay your “welcome tax” when you buy a home? Under which circumstances are reimbursements or exemptions allowed? If you have recently bought a home or condo in Montréal, here’s what you need to know.

Property transfer duties

Property transfer duties, commonly called the “welcome tax,” are a sum of money that all buyers must pay after buying property. If several people buy a building together, they share responsibility for paying these duties.

You must pay your taxes in one instalment within 30 days of the billing date on the tax account invoice.

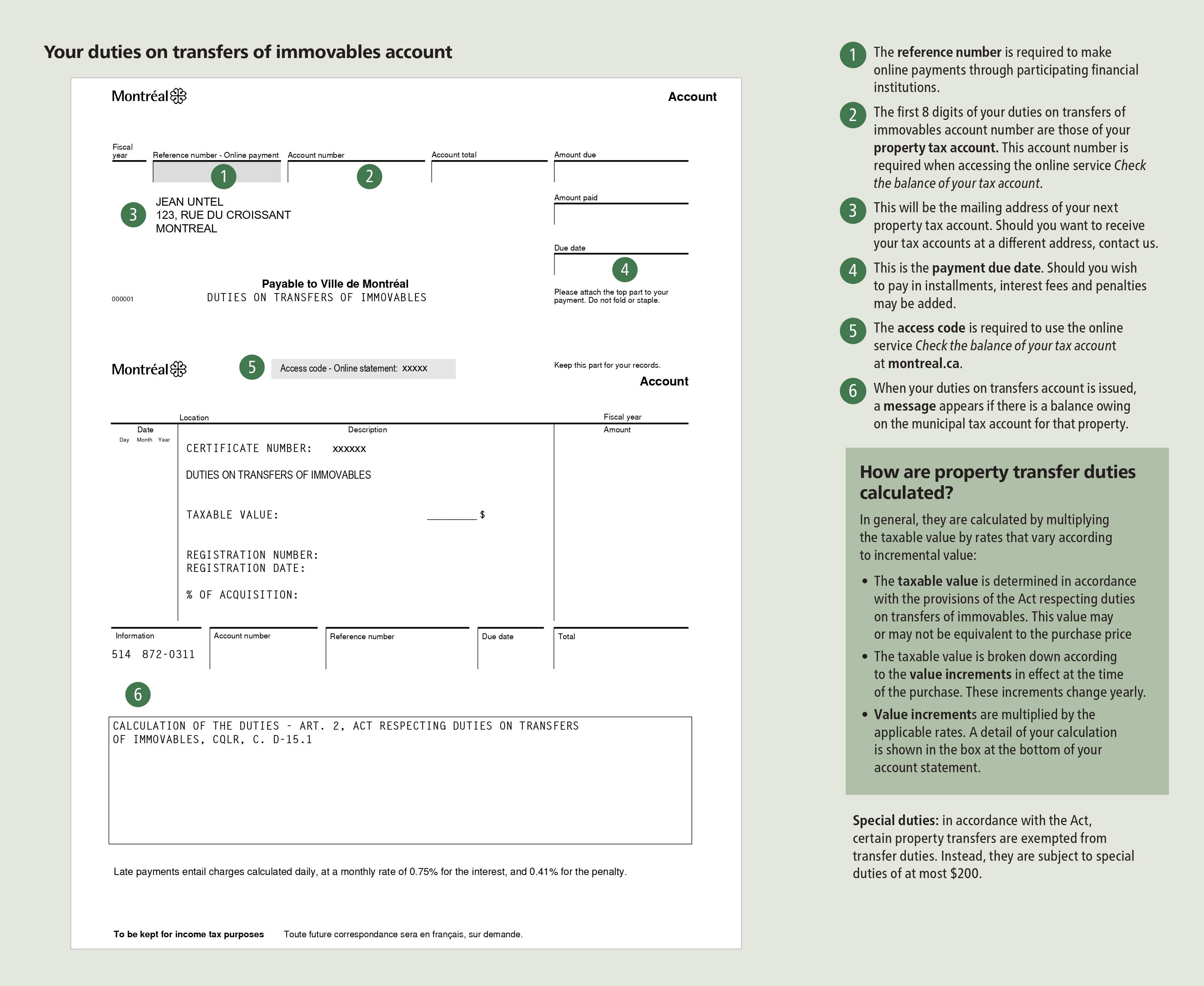

Elements of you account

Your account includes the following elements:

- Reference number

- Payment due date

- Access code required to use our online services

Possible exemption

In some cases, the usual amount of property transfer duties is waived for buyers. This is known as an exemption.

An exemption may be applicable to some transactions:

- Between members of the same family

- From a physical person to a legal entity (company, organization)

Annual tax account

As a new owner, you are responsible for paying property taxes. Tax account invoices are usually mailed out at the end of January each year. They are payable in one or several instalments.

Generally, when the building is sold, the notary calculates the division of tax payment for the current year between the buyer and the seller.

The city does not re-issue a tax account when a building is sold. It is the responsibility of the new owner to ensure that municipal taxes are paid.

Learn more about the topic

How-tos

Programs and initiatives

Need help?

Contact us if you have questions.